9 Small Business Finance Tips For Growth [An Effective Guide]

A small business owner’s life revolves around their business. Therefore, they need to understand what’s going on financially and know how to handle the cash flow. This is where the liquidity ratio comes in – it’s a financial metric that helps you understand your business’s ability to pay its bills.

Knowing your liquidity ratio can help you prioritize your payments, stay on top of expenses, and make intelligent decisions when money is tight. Understanding these terms won’t take long, but it will make a big difference in your business’s long-term health.

Understanding Liquidity Ratio and Why It Matters

When it comes to business, one of the most important metrics is the liquidity ratio. This financial metric helps determine how easily a company can meet short-term financial demands. A low liquidity ratio indicates that the company may have difficulty meeting these demands in the future.

Conversely, a high liquidity ratio signals that a company is ready and able to meet short-term financial needs. It also helps determine how easily a company can sell the stock, borrow money, or refinance debt. So understanding this metric is critical for businesses of all sizes!

What is the Liquidity Ratio?

A low liquidity ratio is problematic as it means that you will need to raise more money or find a way to cut costs in order to stay afloat. On the other hand, a high liquidity ratio signals that your business can quickly meet its financial obligations.

So, monitor your liquidity ratio regularly and take appropriate action if it starts decreasing.

Why is the Liquidity Ratio Important?

The liquidity ratio is an important financial metric that reflects a company’s ability to raise money quickly, creditworthiness, and overall health. For example, a low liquidity ratio can mean that the company has difficulties raising funds or is in debt up high. In contrast, high liquidity indicates healthy finances and strong credit ratings.

How to Calculate Liquidity Ratio

The liquidity ratio is a financial metric that helps investors understand how well a business can repay its short-term debts. It’s calculated by dividing the company’s cash and debt obligations by the total value of its assets.

A high liquidity ratio indicates the business has enough money to cover its immediate liabilities and future payments. Hence, it is an essential indicator of a company’s financial health.

Tips on How to Improve Liquidity Ratios in Your Small Business

Improving liquidity ratios in your small business is vital for several reasons. By following these tips, you can achieve better results:

- Raising money by selling shares or issuing bonds will improve your financial strength and raise the value of your business.

- Reducing debt levels either through cost cutting or borrowing less money will help improve liquidity ratios.

- Boosting capital by issuing new shares or bonds, as well as selling assets, all go to improving the overall health of your company.

4 Tips for Avoiding Common Business Financial Missteps

Creating a business is an exciting and daunting task, but it’s also possible to make some common financial mistakes that can set you back. When establishing financial goals, it’s essential to keep in mind your startup phase when expenses are usually lower and growth phase when costs typically increase.

It’s also helpful to track your progress regularly; this will help you identify areas where you need to adjust your expenditure or save money. Don’t overspend on office supplies or new equipment; try automating tasks or taking advantage of economies of scale by using business loans.

Make use of business tools like invoicing software and marketing automation platforms to run your business more efficiently and effectively.

1. Know What You’re Owed

Understanding your business’s financial standing is essential before making any significant decisions. This way, you’ll be able to make informed and responsible choices that will help the company grow sustainably.

Make sure you have a plan for growth – failure to do so could lead to unforeseen consequences, which can be costly. It’s also crucial that you review your finances regularly and identify areas of improvement – this will allow you to improve cash flow and keep risks under control.

2. Understand Your Monthly Expenses

Managing your small business finances is no easy task. However, with the help of budget software or a spreadsheet, it becomes much more manageable. By keeping track of expenses and making sensible financial decisions, you can ensure that your business runs smoothly and stays afloat in tough times.

One common misstep small business owners make is not accounting for all their costs, including everything from marketing activities to office supplies. Making sure to itemize every expense will also give you a better understanding of where your money is going (and which areas could be cut back).

It’s important to stay on top of changes in the economy so you don’t struggle financially due to unexpected circumstances.

3. Stay Organized and Keep An Eye On The Numbers

Being successful with content marketing takes time, effort, and a good amount of organization. It is important to adhere to some basic principles to stay on track and make sure you are making the most out of your efforts.

For example: Make a budget and stick to it no matter what – even when money is tight. Keep track of all expenses as they can help indicate where potential savings could be made. Also, keep an eye on business debt levels; if things look too precarious or unmanageable, consider consulting an accountant or financial advisor for advice and assistance in sorting everything out.

Finally, having clear goals and setting metrics always helps measure progress along the way, which motivates you further!

4. Get A Credit Score And Avoid Bad Loans

Credit scores are essential for all small business owners, and it is necessary to have a good score when it comes to credit loans. By checking your credit report regularly and ensuring that there aren’t any outstanding debts, you can avert bad financial decisions in the future. It’s also important to remember that planning affects everything – by knowing where you stand financially right now, you’ll be in a much better position to make informed choices when selecting lenders or negotiating terms with them. Additionally, hiring an advisor who specializes in small business finances will ensure that all of your figures add up correctly and help give you more clarity on what steps need to be taken next.

Understanding Debt Ratios and Why They Matter

There are a various terms and numbers flying around when it comes to finances, but few of them are as crucial as debt ratios. Understanding your debt ratios is an essential step in understanding how you’re doing financially.

By calculating your total liabilities and total assets, you can get a sense of where you stand financially. Then, compare this information to your past financial data to see if there has been any change.

This information can also be used to make informed decisions about how to handle your finances moving forward.

What to Look For in a Good Debt Ratio?

When it comes to financial stability, a good debt ratio is essential. It’s important to remember that this number doesn’t accurately reflect the overall health of your finances; there are other factors to consider.

Creating a solid plan for repaying debts and staying on track can improve your credit score. Make sure the debt you’re taking on won’t be too much of a burden in the long run. Your lenders may require proof that the borrowed money will be used productively.

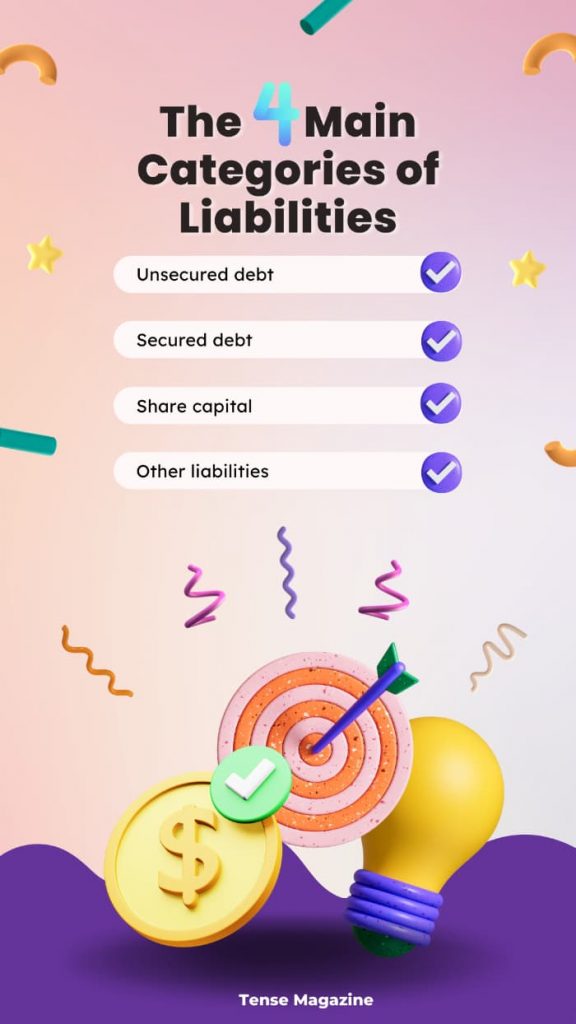

The Four Main Categories of Liabilities

When calculating a company’s net worth, it is important to consider all its liabilities. There are four main categories of liability:

- Unsecured debt (typically has a higher interest rate and shorter repayment period),

- Secured debt (with substantial collateral backing it),

- Share capital (used to finance the growth of the business), and

- Other liabilities.

Understanding these ratios can help you make smart financial decisions to sustain your business over time, whether investing more money in secured debt or issuing more shares for investors.

At the same time, being aware of potential risks associated with each type of liability is essential, so you know how much cushion you have should something go wrong.

Why be Concerned About Debt Ratios?

Debt ratios are a crucial measure of how financially stable a business is. A high debt level indicates that the company might not be able to cover its expenses in the future and could go bankrupt.

Make sure you are reducing your company’s debt levels, so it doesn’t get into this position in the first place. To determine whether your business’ debt ratio is on-point, use several methods such as loan repayment history or cash flow analysis.

Whatever process you choose, regularly review it and take necessary steps to bring it down if needed.

How to Calculate Your Debt Ratio

Debt ratios are a great way to understand your current debt situation and make informed decisions. They allow you to compare different loans/investments in terms of interest rates, loan amounts, etc.

Once you have your debts and assets, you can easily calculate your debt ratio. To do this, simply divide your total debts by your total assets. The ratio that you get will be a percentage.

For example, if your total debts are $50,000 and your total assets are $100,000, your debt ratio would be 50 percent. Knowing your debt ratio can help you determine how much debt you can manage, and how much you need to pay down. It can also help you understand how lenders view your financial profile.

The Importance of Business Budgeting

Without a business budget, you’ll never be able to make sense of your financial numbers. Even small businesses can benefit from creating and tracking one.

Tracking each category regularly will help you understand your performance and adjust as needed. Setting realistic goals and creating a timeline for reaching them is also essential. This way, you won’t get discouraged when obstacles or delays arise.

It’s crucial not to overspend on any given category- otherwise, your business might not survive long term! Create categories within your budget for paying bills, advertising, and other expenses.

This will help keep everything organized and manageable – making it easier to stay on track while managing cash flow issues or unexpected expenses. And finally, don’t forget that financial planning is an ongoing process; don’t wait until things become dire before taking action!

Make Proper Investments

When it comes to making proper business investments, there are a few things you need to keep in mind.

Firstly, cause sure your budget is realistic and achievable. Then, once you have done that, track progress to see where improvements or changes are needed. Don’t forget future expenses – they will play an essential role in shaping your business’ long-term prospects and profitability.

A business budgeting system can help streamline this process considerably by considering all these factors. By doing so, you’ll be better equipped to make sound financial decisions for your company’s future.

Track Your Revenue

Keeping track of your business revenue is crucial to make informed decisions and staying on track. Here are a few tips to help you achieve this:

- Always understand your income and expenditure to know where money is going and what needs to be trimmed down.

- A business budget will help you better understand how much money has been generated each month and plan future expenses accordingly.

- Use budgeting software – there are many available online, which makes the task more accessible and more manageable.

- Just enter all the relevant data at once instead of tracking it separately every time expenses arise or Income fluctuations occur.

This way, you’ll always be up to date with everything! Don’t forget to save enough money each month if something unexpected (i.e., a health emergency) pops up. By doing these four small things consistently over time, it becomes MUCH harder for businesses to run into problems due to cash flow issues!

Understand Your Costs

Managing your business finances is an essential aspect of any successful endeavor. Without a solid grasp on expenses and revenue, making informed decisions when planning for the future or cutting costs to reach profitability will be hard.

You can track your spending in various ways – perhaps using a cash flow tracker or Profit & Loss spreadsheet. Once you understand where the money goes, breaking it into categories like marketing software, operations, R&D, etcetera becomes much more accessible. It’s also essential to create detailed budget forecasts so that you know how much money is available each month and whether any funding gaps are needed for long-term growth plans.

The first step towards good business financial management is learning about your costs! Often this information isn’t readily accessible or easily calculable, leading to inaccurate assumptions about what needs to be spent and on what initiatives.

Make Intelligent Decisions When Investing in Your Business

When making decisions about your business, you must understand the impact of taxes and fees. For example, if you buy a business asset such as equipment or software, consider the associated tax and fee costs.

Another financial decision that is important to make is financing your business. You can save money on interest rates down the road by using cash instead of borrowing. However, when looking for long-term financing options, remember that interest rates vary based on credit score and other factors.

It’s always most suitable to do your homework before making a final decision. Don’t overspend when starting – your first investments should be low-cost items like a computer and internet access. This way you won’t have any problems when trying to fund more expensive purchases in your busines.

Protect Yourself From Financial Risks

You are taking proper financial precautions when starting or running a business is essential. Make sure you have a well-thought-out plan and track your progress regularly to know where you stand.

You must also save money frequently and keep an emergency fund if unforeseen costs arise. Finally, bear the financial risks involved before doing anything, as making ill-informed decisions could have devastating consequences.

Understand Your Depreciation Scheme

It’s essential to understand your depreciation scheme to make sound financial decisions. This is especially relevant regarding assets such as machinery and equipment, which can have a long lifespan.

To determine the length of time investment will last, you need data on current performance and average life expectancy for the same type of product or technology. Once this information is available, you can start making accurate estimates about how much money will be spent on replacement/maintenance over its lifetime.

In addition, consider the cost of replacing old equipment with new models that offer better efficiency – both from a financial and environmental perspective!

Calculate Tax Liability Accurately

When it comes to business finances, accuracy is critical. That’s where the Taxable Income Calculator comes in handy. It will help you calculate your tax liability accurately and make intelligent decisions when refinancing or borrowing money for growth purposes.

It’s also important to keep an eye on business liabilities and assets – this can help you better gauge whether a particular financial decision is wise. Using the Profit & Loss Calculator to track changes in profitability over time-this will give you a more accurate picture of your business’ health overall.

Know Your Expenses and Profits

Running a business is an expensive and time-consuming task. It’s important to stay on top of expenses and profits to make the right decisions for your business. Comparing your interaction with others in the same industry will give you a good idea of where you stand and help you better understand customer needs.

Educate yourself about finance by reading articles, watching videos, or attending seminars; this way, you’ll be able to grasp complex concepts and make sound judgments regarding money management.

It would also be beneficial to track expenses and profits over time in order not only to monitor financial growth but pinpoint areas of improvement too. By doing so, businesses can get a comprehensive understanding of their cash flow dynamics which will help them identify potential problem spots earlier – preventing them from becoming unmanageable later down the line!

Understand Your Profit and Loss (P&L) Statement

To stay on track and grow your business, it’s important to understand your P&L statement. This document tells you how much money the company made and lost in each category over the past few months or years.

Remember, it’s important to stay disciplined with your spending so you can grow your business! A P&L statement is a great way to understand your business’ finances. By understanding where funds are being spent, you can decide better where to allocate resources next.

What is a P&L Statement?

A P&L statement is a snapshot of your business’s financial performance over time. It gives you an overview of where money has been earned and spent, helping you identify which areas need improvement so your business can reach its financial goals.

Once you understand this information, making the necessary alterations to your operations becomes much more accessible.

How to Read Your P&L Statement

Understanding your company’s financial health is an essential part of business decisions. For instance, you can use a P&L statement to make informed decisions about raising capital or selling shares.

Knowing how much money your business has made and lost in the past helps you plan for future growth or recessionary periods. Profit and loss inform all levels of management on where their business stands – from top executives to frontline staff.

The Different Sections of a P&L Statement

Understanding each section of a business’ P&L statement is vital in making informed decisions. This financial document can evaluate your business performance over a certain period and identify areas where improvement is needed.

You need to be aware of some critical ratios of our EBITDA (Earnings Before Interest, Taxation, Depreciation, and Amortization), Net Income, etcetera. The different sections of the P&L statement usually include income, expenses, and equity.

Analyzing Your Profit and Loss (P&L) Statements

Profit and loss statements are a valuable tool for business owners to use to understand their performance over a certain period. By analyzing these statements, you can understand where your business is making money and where it is spending money.

This information can be beneficial when planning future moves or assessing whether you are on track with the business’s overall financial strategy. If possible, you should also break down your P&L statement by category to get an even more detailed picture of your financial health. This will help identify any potential areas for improvement or expansion.

Making Decisions Based on Your P&L Statements

Making decisions that align with your business’s profits and losses is essential. To do this, you can use your P&L statements to assess your business’s financial standing. This information will help you decide which areas of your business need more attention and resources.

It can also be used to fine-tune the marketing strategies of different segments of your company. Doing so ensures that all customer touchpoints are practical and relevant, driving better results for both short-term profitability and long-term growth prospects.

Track Expenses Against Income

Are you wondering where your money is going and whether or not you’re on track to achieve your financial goals? Use a budgeting software program to help create realistic goals and track progress.

This document will help you understand where your money is going and how you can save money. Another helpful tool for tracking expenses against income is a cash flow statement. This report shows how much cash was brought in and how much money was spent over a specific period.

Understanding these metrics allows you to make better business decisions that will ensure long-term success. Having good financial information will also make it easier to deal with day-to-day finances stress-free!

Understanding the Difference Between Net Income and Profit Margin

The business world is constantly changing, and so are how expenses and income are tracked. To remain competitive, it’s important to keep up with these changes. Here’s a quick look at how profit margin and net income work:

- Net Income = Revenue – Expenses

- Profit Margin = Net Income / Revenue

You want your profit margin to be as high as possible because that means you’re making more money from every sale than what was spent on revenue generated from those sales (i.e., there’s been an excess of cash flow).

This helps your business stay afloat during tough times while allowing for future growth potential.

Assessing Where Your Money Goes

It is essential to assess where your business’ money goes so that you can make informed decisions about how best to allocate it. This includes looking at your Profit and Loss Statement, examining which marketing or equipment expenses are necessary, and figuring out ways to reduce costs without compromising quality or service.

Once these assessments have been completed, tweaks and adjustments may be required for the business to thrive long-term.

Analyzing Your Profit and Loss Statement

One of the most critical steps in effective business management is knowing your profit and loss statement. It can help you identify discrepancies and decide when it would be appropriate to take on new debt or reduce expenses.

By tracking your expenses against your income, you will also understand where money is being misallocated – this could lead to a corresponding savings account!

Calculating Taxable Income

An excellent way to calculate your taxable income is by tracking expenses against income. This will help you identify where you are overspending and save money in the long run.

Once you have identified this, making changes and saving money on your monthly expenses becomes much more accessible. In addition, compare what data you have collected with your annual income to see where there might be room for improvement.

By doing so, not only will finances become more manageable, but also your financial planning can get a lot more accurate!

Preparing Your Tax Returns

There are a lot of things you need to take into account when preparing your tax returns. Check our website for tips and advice on the best way to go about it! Additionally, tracking expenses is essential to show how much money you’re spending each month accurately.

After all, knowing where your cash goes will make filing taxes much more straightforward. Finally, working with a financial planner or software can streamline the entire process – they’ll be able to identify any deductions and credits that may apply based on your income and expenses.

Establish a Budget and Stick to it

When starting a small business, it’s essential to have a clear understanding of your monthly expenses. This will allow you to track where your money is going and help you make informed decisions about allocating resources.

First and foremost, establish a budget and stick to it. This will help you keep tabs on your spending and ensure that each dollar goes towards achieving goals instead of frivolous items. Additionally, explore different financing options – from loans to equity investments – for your business to thrive in the future.

It’s helpful to look at past financial statements to get an idea of how profitable or unprofitable your business is. By doing this, you’ll be able to determine whether or not refinancing is necessary and which areas need more attention for growth potential to exist within the company.

Stick to One Source of Funding

Keeping small business finances organized is vital for success. One of the most influential things you can do to achieve this goal is to stick to one source of funding – your budget. Next, make sure that your budget reflects all your business’s expenses and doesn’t exceed what you can pay back reliably.

Once you have established a firm financial footing, weathering any unexpected cash flow problems or economic downturns will be much easier. Lastly, make sure each expense is accounted for and justified in order not to let personal biases or misconceptions creep into decisions about spending money on behalf of your business.

Know Your Costs

It will be challenging to make informed business decisions without knowing your costs. It is equally important to stay within budget no matter what the financial situation may be like. Armed with accurate figures and information about your income and expenses, you can begin making rational decisions that would help keep your business afloat during tough times.

Establishing a budget should not only be done when things are going smoothly – sticking to it should become part of your daily routine, even during periods of turmoil or high turnover rates. This way, you’ll know exactly how much money you’re taking in (and spending) every month without any guesswork involved.

Set Milestones and Make Sure You Hit Them

A plan is essential to know exactly where you are heading and your goals. This way, there is little room for error, and everything proceeds smoothly from start to finish.

Along with planning, tracking expenses is also essential – this will help identify areas that can be cut down or economized. Keep numbers conservative while still hitting your targets; overestimating can lead to big financial losses later on. Ultimately, it pays off to take the time needed up front rather than rushing things along and making costly mistakes later on!

Pay Yourself Regularly

When it comes to money, most of us are guilty of blowing through our budgets without batting an eyelid. But why do we struggle so much with budgeting in the first place?

Sure, breaking habits that have become second nature is not easy, but if you want to achieve financial stability and avoid unnecessary stress, following a routine is essential.

To make things easier for yourself, review your monthly expenses and look for areas where you can save cash. It’s also advisable to automate your finances as this will help reduce the number of hassles associated with financing activities such as bill payments or credit card statements. And lastly – always keep a budget in mind!

This way you’ll be able to plan your spending and stick to it even when times get tough.

Use Budgeting Tips from Experts

Setting and sticking to a budget can be difficult, but it is essential for financial stability. That’s why it is always recommend to consult experts when planning your finances. Here are four tips that will help you create a realistic budget:

- Don’t be tempted by flashy ads or sales pitches – Stick to what you can afford, and don’t overspend.

- Make sure your spending spree doesn’t snowball into more significant problems – Have an emergency fund in case of unforeseen expenses.

- Prioritize your purchases according to their importance so that you know where money is going – This will help keep wasteful spending under control.

- Use budgeting tips from experts who can guide how much money specific items should cost and advice on creating adequate budgets overall.

Save for Future Growth & Expansion

No business is ever risk-free, but it’s essential to try and minimize the risks as much as possible. One way to do this is by saving for future growth and expansion. Begin by setting aside a percentage of your income each month to keep.

This will help you accumulate money over time, which can be used for anything from expanding your business venture to financing new acquisitions or investments. Next, make sure you take advantage of all the tax breaks available to small businesses (like the startup expensing provision).

And diversify your investments, so you’re not putting all your eggs in one basket – this will help protect your money from volatility.

Make a Plan to Save Regularly

Saving is an essential part of business growth. However, it can be challenging to stick to a budget when there are so many expenses to account for. That’s why tracking your costs and making use of tax breaks, and financial incentives are essential.

Aiming to save around three-six months’ worth of expenses will help you cover unexpected costs or make necessary investments in your business. By following a plan, you’ll achieve more tremendous success in reaching your savings goals over time – something that definitely warrants taking action!

Diversify Your Income Sources

Having multiple income sources is a great way to reduce your vulnerability to any one financial setback. By diversifying your business, you can also be more proactive in case of an emergency and increase the chances of success overall.

There are many creative ways companies can generate extra income such as conducting a paid search or creating an online course. It’s important to remember that long-term growth opportunities will always outshine quick fixes so make sure you save regularly and invest wisely for the future!

Keep Your Business Expenses Under Control

Running a business is expensive, and spending more money is easy than you initially thought. It’s essential to be vigilant about every penny you spend and make sure all expenses are carefully scrutinized.

Even the smallest costs can add up quickly, so it is necessary to track your finances using budgeting software or Apps regularly. It’s also beneficial to automate your finances as much as possible – this will help you stay within your financial limits while allowing you not to have stress over small money matters anymore.

Lastly, Saving for future growth should always be at the top of your list when planning budgets – even if things seem tough right now! This way, businesses can prepare themselves for anything that might come their way down the line.

Stay Flexible with Pricing & Terms of Services

Taking time to plan your finances and stay flexible with pricing & terms of services is important in avoiding financial ruin. Being too rigid can lead to a reluctance by customers to pay on time, leading to cash flow issues.

It’s essential that you maintain good customer relations – this means being willing or able to adjust prices & terms as needed without resentment from the customer base. Growth & expansion should never come at the expense of margins or profitability; make sure you have a business model in place that will allow for these luxuries. Don’t let debt take over your life!

By following these simple tips, you’ll be well on your way towards financial stability and long-term happiness.

Evaluate Potential Investments for Long-Term Sustainability

It is essential to have a long-term financial plan in place so you can make smart investments that will benefit your business over time. However, this doesn’t mean you should be afraid of making mistakes.

An excellent way to overcome any uncertainty or fear would be to ask for help from a financial advisor who can provide unbiased advice and steer you in the right direction. When evaluating potential investments, ensure not just their short-term return but also their sustainability is taken into account. Is the investment likely going to provide a long-term recovery?

Will it stand the test of time? Putting together these considerations will help keep your finances on track and allow you to stay confident about your decisions overall.

Frequently Asked Questions

Should I open a bank account for my small business?

Opening a bank account for your small business is often a good idea as it can provide several benefits, including easier bookkeeping, access to loans, and protection from financial risks. However, there are no restrictions on which bank you can open an account with, so feel free to choose whichever meets your business needs.

In terms of the minimum balance requirement, small businesses usually require around $500 as a minimum deposit. This amount will vary depending on the bank but is generally very small compared to the total loan amounts available to small business owners.

What is a due-diligence check, and what does it entail?

A due-diligence check is a routine financial health check that helps to identify any red flags and potential issues with your business. This includes checking for tax liabilities, verifying ownership of assets, and conducting audits to ensure your finances are in order.

Typically, this check will take around 2 hours to complete but it’s essential to have it done regularly so you can detect problems early on. In addition, doing this will help avoid any nasty surprises down the road and keep your business afloat and healthy.

How can I calculate my net worth and assess my capital needs?

To calculate your capital needs, you’ll need to understand your business goals. Are you starting a business from scratch, or do you have an existing business that you want to improve? Once you’ve determined your business goals, you can begin to figure out how much money you’ll need to get started. There are three main components of your net worth – assets, liabilities, and equity.

- Your assets are anything that has a cash flow or value that supports your business operations.

- Your liabilities are anything you owe someone else – like credit card debt, student loan debt, or car loans.

- Equity is left once everything is accounted for and divided among all the stakeholders.

How do I deal with significant financial numbers when running my small business?

When running a small business, one of the most important things you can do is understand your finances. This begins by breaking down your expenses into costs (things you pay for) and income (the money you earn). Once you better understand where your money is going, it will be much easier to make intelligent financial decisions.

Bottom Line

Making sense of big financial numbers can be a daunting task, but with the help of these nine small business finance tips, it will be much easier. By understanding liquidity ratio and other key financial metrics, you’ll be able to make informed decisions about your business finances.